How to Pay for Memory Care in Cleveland: A Guide for Ohio Families

-

TL;DR: The average monthly cost of memory care in the U.S. is around $7,908. Most families in the Cleveland area pay for it using a combination of private funds (savings, home sale), long-term care insurance, and public benefits like VA Aid & Attendance or Ohio's Medicaid Assisted living Waiver.

-

Ohio's Medicaid Assisted Living Waiver helps pay for care services but not room and board. It's a key resource for making care affordable long-term.

-

Medicare does not pay for long-term memory care. It only covers short-term skilled nursing after a qualifying hospital stay.

-

Start by getting a complete picture of your loved one's finances and consult an Ohio elder law attorney before moving any assets.

Who This Helps

This guide is for families in Greater Cleveland (including Cuyahoga, Lake, Lorain, Geauga, Medina, and Summit counties) who are trying to understand how to afford memory care for a loved one. We know you're likely stressed and short on time, so this guide provides clear, practical steps to build a financial plan.

Key Takeaways

-

Memory care costs include a base rate, level-of-care fees, and one-time fees. Always ask for a full cost breakdown.

-

Most families use a mix of funding sources, starting with private savings, retirement funds, or the sale of a home.

-

Long-Term Care insurance can be a major help, but you must understand its "elimination period" (a waiting period before benefits start).

-

Ohio-specific programs like the Medicaid Assisted Living Waiver (AL Waiver) and federal VA benefits can significantly reduce your monthly out-of-pocket costs.

Understanding Memory Care Costs in Cleveland

When a memory care community gives you a price quote, it's rarely a single, all-in number. The total monthly bill is usually made of a few different parts. Understanding these pieces is essential for comparing your options and avoiding financial surprises.

The higher cost of memory care compared to standard assisted living reflects the specialized support required for someone living with dementia. This includes:

-

Higher Staffing Ratios: More staff members are needed to provide safe, 24/7 care and supervision.

-

Specialized Training: Care staff receive ongoing training on how to manage behavioral symptoms of dementia with compassion.

-

Secure Environments: Communities invest in safety features like secured courtyards and key-coded elevators to prevent wandering.

-

Purposeful Programming: Activities are designed by specialists to engage residents, reduce agitation, and support cognitive function.

The Three Main Components of Your Bill

Think of the monthly bill in three layers. This framework helps you ask the right questions during tours.

1. The Base Rate: This covers the essentials: the apartment or suite, three meals a day, utilities, housekeeping, laundry, and access to general community amenities and social programs.

2. Level-of-Care Fees: This is an additional fee determined by a clinical assessment of your loved one's specific needs. It covers hands-on help with "activities of daily living" (ADLs) like bathing, dressing, managing medications, and mobility. As needs change, this fee will likely adjust.

3. One-Time Fees: These are upfront costs you pay when moving in. The most common is a "community fee," which covers administrative work and apartment preparation. Always ask if this fee is refundable.

What this means for you: When you're comparing communities in Cuyahoga or Lake counties, always ask for a full cost breakdown. A community with a lower base rate might look appealing, but if its level-of-care fees are high, the total monthly bill could be more than a community with a higher, more inclusive base rate.

Realistic Costs in Northeast Ohio

While prices vary by location and amenities, families in the Greater Cleveland area should budget for a significant expense. For a deeper look at the numbers, our guide on how much memory care costs is a helpful resource.

According to recent national data, the average monthly cost for memory care was $7,908 as of March 2025. This is more than assisted living but generally less than a skilled nursing facility, which is regulated by the Centers for Medicare & Medicaid Services (CMS) and provides a higher level of medical care.

Typical Memory Care Cost Breakdown in Northeast Ohio

This table shows how costs might break down in our local area, giving you a clearer picture of what you're paying for.

| Cost Component | Description | Estimated Monthly Cost Range (Cleveland Area) |

| :--- | :--- | :--- |

| Base Rate | Covers rent, meals, utilities, and basic amenities. | $4,500 – $7,000 |

| Level-of-Care Fees | Varies based on personal care needs (e.g., medication management, bathing assistance). | $500 – $2,500+ |

| One-Time Fee | A non-recurring fee paid at move-in for administration and apartment prep. | $1,500 – $5,000 |

Note: Last Updated March 2025. These are estimates. The only way to know the exact cost is to get a personalized quote from the communities you are considering.

Starting With Your Own Resources: Private Pay & Insurance

For most families in Northeast Ohio, the first step is to review personal financial resources. This is known as "private pay" and is the most direct way to cover memory care costs. It requires careful planning but gives you the most control over your choices.

Common sources for private pay include:

-

Savings and Investments: Cash in checking or savings accounts, stocks, bonds, and mutual funds.

-

Retirement Funds: Money from 401(k)s, IRAs, and pensions.

-

Annuities: These can provide a reliable, steady income stream to help cover monthly costs.

Before moving large sums of money, consult a qualified financial advisor to understand any tax implications.

Using a Long-Term Care Insurance Policy

If your loved one has a Long-Term Care (LTC) Insurance policy, now is the time to locate that document. These policies are designed for this exact situation, but activating benefits requires a few steps.

First, you need to understand the elimination period. This is a waiting period—often 30, 60, or 90 days—that you must pay for care out-of-pocket before the insurance company begins payments.

To start a claim, you'll need a doctor to certify that your loved one needs help with at least two "Activities of Daily Living" (ADLs)—like bathing, dressing, or eating—or has a severe cognitive impairment like Alzheimer's.

Example: A Cuyahoga County family using LTC insurance

A family in Parma had a father with an LTC policy that had a 90-day elimination period and a $200 daily benefit. After his doctor confirmed he needed memory care, the family paid privately for the first three months. On day 91, the insurance payments began, covering a large portion of the monthly bill and providing significant financial relief.

Tapping Into Home Equity and Life Insurance

Other major assets can also be used to fund care. These options can unlock significant funds but involve important decisions for the whole family.

Selling the Home

For many seniors, their house is their largest asset. Selling it can free up enough money to cover care for several years. This is a common strategy, especially if a surviving spouse is not living in the home.

Reverse Mortgage

This is a loan for homeowners age 62 and older that allows them to borrow against their home’s value. The loan is repaid only when the home is sold or the owner moves out permanently. It can be a solution for a couple where one person moves into memory care while the other remains at home.

Life Insurance Conversion

Some life insurance policies have a cash value you can borrow against. Another option is a "life settlement," where you sell the policy to a third-party company for more than the cash surrender value but less than the final death benefit.

Checklist: How to Activate an LTC Policy

Having your paperwork organized will make the claims process much smoother.

-

[ ] The Original Policy Document: This details your benefits, daily payment caps, and the elimination period.

-

[ ] Physician's Certification of Need: A formal letter or form from the doctor detailing the diagnosis and why your loved one needs this level of care.

-

[ ] Community Admission Agreement: Proof that your loved one has officially moved into a licensed care community.

-

[ ] Initial Invoices: Copies of the first few monthly bills to prove you are paying for care during the elimination period.

-

[ ] Power of Attorney (POA) Documents: The insurer will need a copy of the financial POA to work with you on your loved one's behalf.

To cover gaps in primary insurance, supplemental insurance plans may help with co-pays or other expenses not covered by an LTC or standard health plan.

Navigating Ohio's Public Benefit Programs

When private funds and insurance don't cover the full cost, public benefit programs can be a lifesaver. For families in Ohio, understanding these state and federal resources is a critical step. The rules can seem complex, but the key programs are straightforward once you know the basics.

The economic reality of dementia care is significant. In the U.S., the total cost is projected to reach $781 billion in 2025, with much of that paid by Medicare and Medicaid, according to dementia care research. These figures highlight the vital role of government programs.

The Medicaid Assisted Living Waiver: A Closer Look

In Ohio, one of the most important programs is the Medicaid Assisted Living Waiver (AL Waiver). This is different from traditional Medicaid that pays for nursing homes. The AL Waiver is specifically designed to help eligible seniors receive care in an assisted living setting, which includes many memory care communities (licensed in Ohio as Residential Care Facilities).

Here’s the most important thing to know: in Ohio, the AL Waiver pays for care services, not room and board. The program covers costs for personal care, medication management, and nursing oversight. The family remains responsible for the community's base rent for the apartment and meals.

To qualify in Ohio, an individual must generally meet three conditions:

-

A Medical Need: A doctor must confirm they require a "nursing facility level of care," which is standard for individuals with mid-to-late stage dementia.

-

Financial Eligibility: The individual must meet strict income and asset limits set by Ohio Medicaid. These limits can change, so always check the latest figures from the state.

-

An Approved Community: They must choose a memory care community that is certified by the state to accept the AL Waiver.

What this means for you: The AL Waiver can dramatically lower your monthly bill by covering the "level-of-care" fees, which can add thousands of dollars to the cost. It often makes a quality memory care community financially possible for the long term.

For detailed eligibility rules, you can learn more about how the Medicaid assisted living waiver works in Ohio.

Unlocking VA Benefits for Veterans

If your loved one served in the military or is the surviving spouse of a veteran, don't overlook potential benefits from the Department of Veterans Affairs (VA). The program that most often helps with memory care is the Aid & Attendance pension.

This is a tax-free monthly payment added to a basic VA pension. It is specifically for veterans who need help from another person for daily activities like bathing or dressing—the core needs of dementia care.

The benefit is paid directly to the veteran or spouse, making it a flexible way to help pay the monthly memory care bill. It acts as a new income stream that makes private payment more manageable.

The Truth About Medicare

This is the biggest point of confusion for families. To be clear: Standard Medicare does not pay for long-term, custodial care in a memory care community.

Medicare is health insurance. It covers doctor's visits, hospital bills, and short-term skilled nursing rehabilitation after a qualifying hospital stay (for up to 100 days). It was not designed to cover the 24/7 personal care and supervision that defines memory care. Relying on Medicare for this will leave you with a major coverage gap.

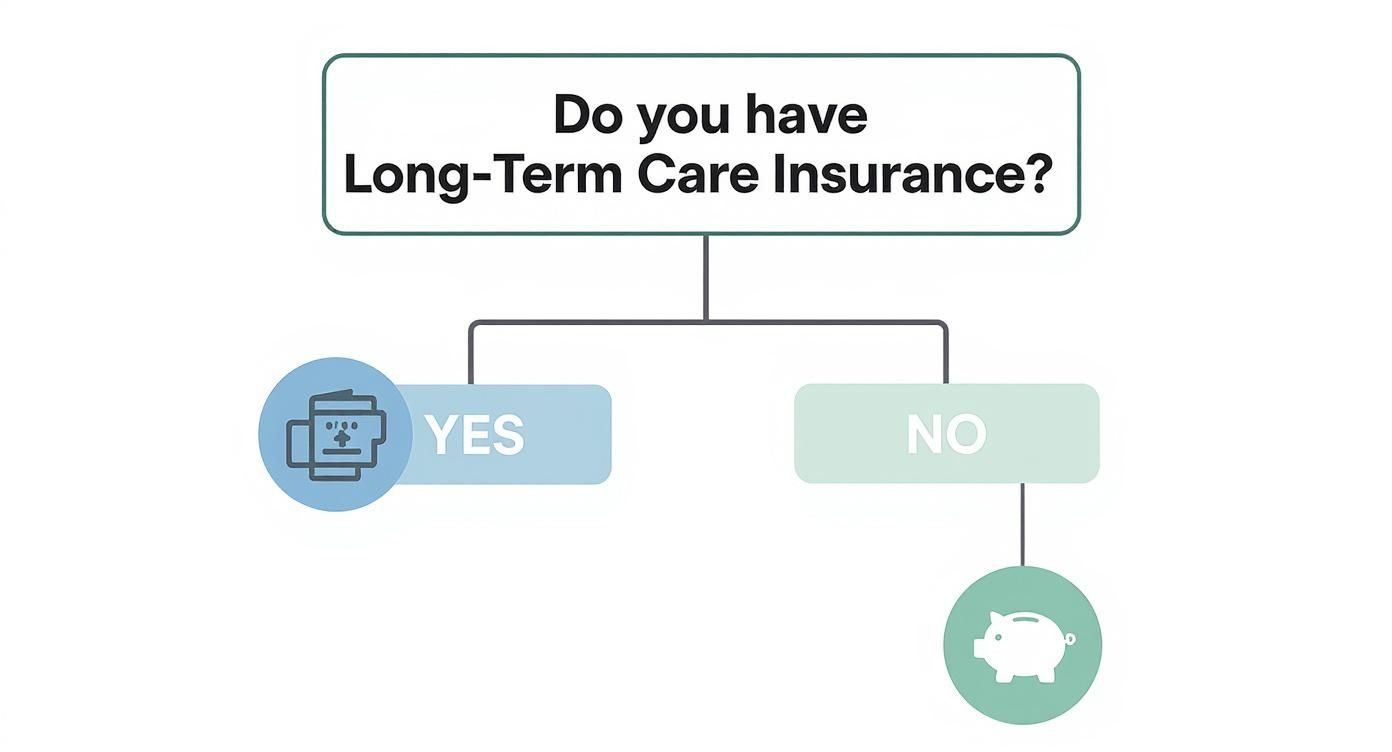

This decision tree shows how to start your financial planning by looking at private insurance before moving to public benefits.

(Alt text: A decision tree diagram showing the financial planning path for memory care. It starts with a question: "Does the person have a Long-Term Care Insurance policy?" If yes, the path leads to "Activate Policy" and "Use Private Pay for Gaps." If no, the path leads to "Assess Private Funds (Savings, Home Sale)," then to "Apply for Public Benefits (VA, Medicaid)" to supplement the cost.)

Your Local Ohio Contacts to Get Started

You don't have to navigate this alone. Northeast Ohio has excellent agencies to help you.

-

For the AL Waiver: Your first call should be to the Western Reserve Area Agency on Aging (WRAAA). They are the designated entry point for these programs in Cuyahoga, Geauga, Lake, Lorain, and Medina counties and will conduct the initial eligibility assessment.

-

For VA Benefits: Contact your county's Veterans Service Commission. They have trained officers who will help you gather documents and file the application at no cost.

Finding Funds for Immediate Care Needs

Sometimes, the need for memory care arises suddenly, leaving families scrambling for cash while knowing they have assets like a home or pending benefits. This timing gap is a common and stressful problem. Fortunately, specific financial tools are designed to bridge this gap.

Using a Bridge Loan for Quick Access to Cash

A bridge loan is a short-term loan that creates a financial "bridge" to cover senior living expenses while you wait for other funds, like the sale of a home or approval of VA benefits, to become available.

These loans are helpful for covering a community’s move-in fee and the first few months of rent. They are often approved quickly based on credit score.

What this means for you: A bridge loan provides speed and convenience but often comes with higher interest rates than a traditional loan. It's best used as a temporary tool for a specific, short-term need.

Understanding the Medicaid Spend-Down Process

If you plan to use Ohio's AL Waiver, you need to understand the term “spend-down.” This is the process of legally spending down your loved one’s assets to meet the strict financial limits for Medicaid eligibility.

This is not about hiding money or giving it away. In fact, gifting assets can trigger Medicaid’s five-year "look-back" period, leading to a penalty period where your loved one is ineligible for benefits.

A proper spend-down involves using excess funds on permissible expenses that benefit your loved one. Getting local guidance is critical; many families find that reputable senior living placement services can connect them with the right financial and legal experts in the Cleveland area.

Your Checklist for a Permissible Spend-Down

In Ohio, your loved one's excess funds can be used for allowable expenses before applying for Medicaid. Common examples include:

-

[ ] Pay Off Existing Debt: Pay off mortgages, car loans, and credit card balances.

-

[ ] Pre-Pay Funeral and Burial Expenses: Purchase an irrevocable funeral trust or burial plot for your loved one and their spouse.

-

[ ] Make Home Modifications for Safety: If a spouse remains at home, use funds for a wheelchair ramp or walk-in shower.

-

[ ] Purchase Medically Necessary Equipment: Buy items Medicare may not cover, like a new wheelchair, hearing aids, or an adjustable bed.

-

[ ] Pay for Dental or Vision Care: Take care of needed dental work or get new eyeglasses.

Always consult an Ohio-based elder law attorney before starting a spend-down. They can provide personalized advice to ensure every expense complies with state Medicaid rules and protects you from costly mistakes.

Building Your Memory Care Payment Strategy

<iframe width="100%" style="aspect-ratio: 16 / 9;" src="https://www.youtube.com/embed/LExoPA4nSn0" frameborder="0" allow="autoplay; encrypted-media" allowfullscreen></iframe>Moving from research to action can be the hardest part. Now it's time to pull all the information together into a clear, personalized financial plan for your family.

The financial strain on families is real. Unpaid caregivers in the U.S. provide billions of hours of care each year. Creating a sustainable financial plan is not just smart—it's essential for your family's well-being. You can learn more about the economic impact of dementia and its effect on families.

Your Memory Care Financial Planning Checklist

Use this checklist to guide your next steps. Tackling these items one by one will make the process feel more manageable.

-

[ ] Gather All Financial Documents: Collect bank statements, retirement account summaries, investment portfolios, and any pension or annuity paperwork.

-

[ ] Locate Insurance Policies: Find original documents for Long-Term Care, life, and health insurance. Note benefit triggers, daily payment amounts, and elimination periods.

-

[ ] Schedule a Level-of-Care Assessment: Contact a few top-choice communities to schedule a clinical assessment. This is the only way to get an accurate, all-in cost estimate.

-

[ ] Contact the Area Agency on Aging: In the Cleveland area, that’s the Western Reserve Area Agency on Aging. This is your first stop for information on AL Waiver eligibility.

-

[ ] Assemble VA Paperwork: If your loved one is a veteran, find their military discharge papers (DD-214) and marriage certificate to apply for benefits like Aid and Attendance.

Document Checklist for Financial Planning

| Document Category | Specific Examples | Why You Need It |

| :--- | :--- | :--- |

| Proof of Identity & Age | Birth certificate, driver's license, Social Security card | Required for nearly all benefit applications (Medicaid, VA). |

| Income Statements | Social Security benefit letter, pension statements, recent pay stubs | Verifies monthly income to determine eligibility for needs-based programs. |

| Asset Information | Bank statements (3-5 years), investment/IRA/401(k) records, property deeds | Provides a full picture of assets for Medicaid's asset test and overall financial planning. |

| Insurance Policies | Long-Term Care Insurance policy, life insurance documents, Medicare/Medigap cards | Details coverage limits, waiting periods, and contact information for filing claims. |

| Military Records | DD-214 (Discharge Papers), marriage certificate | Essential for applying for any VA benefits, including Aid and Attendance. |

| Legal Documents | Power of Attorney (Financial & Healthcare), Will or Trust documents | Clarifies who has legal authority to make decisions and manage finances. |

Putting It All Together

Once you have your information, you can layer different funding sources to cover the monthly cost.

Example: A Geauga County Family's Plan

A family in Chardon determined their mother’s total monthly cost at a local community would be $7,200. They built a plan combining several resources:

- Social Security & Pension: This provided a base of $2,800 per month.

- LTC Insurance: After a 60-day waiting period, her policy paid $150/day, covering another $4,500.

- Covering the Gap: This combination nearly covered the full cost, leaving a small gap of $100/month that the family covered with a planned withdrawal from an IRA.

This shows how a large, intimidating number can become a manageable solution.

What to Do Next

-

Book Community Tours: With a realistic budget, schedule tours at 2–3 communities that fit your financial plan. Ask specifically about their level-of-care fees and if they accept the Ohio AL Waiver.

-

Consult an Elder Law Attorney: Before moving money or applying for Medicaid, speak with a qualified Ohio elder law attorney. Their advice on asset protection and spend-down strategies is invaluable.

-

Hold a Family Meeting: Get everyone on the same page. Share the estimated costs, the payment plan, and discuss how each person can contribute, whether financially or with their time and support.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or medical advice. Please consult with licensed professionals for guidance on your specific situation.

FAQ: Common Questions About Paying for Memory Care

Here are answers to some of the most common questions we hear from families in the Cleveland area.

Can We Just Give Away Mom's Assets to Qualify for Ohio Medicaid?

No. This is a common misconception that can lead to serious penalties. In Ohio, Medicaid has a strict five-year "look-back" period. When you apply, they will review all financial transactions for the last 60 months. If they find large gifts or assets sold for less than fair market value, they will impose a penalty period, delaying benefits for months or even years. During this penalty period, you would have to pay the full cost of care out-of-pocket. Before moving any assets, your first step should be to consult an Ohio-based elder law attorney.

What if My Dad Runs Out of Money While He's in Memory Care?

This is a valid fear. The best approach is to be proactive. If you foresee that your loved one's funds will be depleted, schedule a meeting with the community's administrator immediately. The most common solution is to apply for the Ohio Medicaid Assisted Living Waiver. If your loved one meets the financial and medical criteria, the waiver can step in to cover the cost of their care services, allowing them to remain in the community. They may need to move to a Medicaid-certified room. Open communication with the community staff is key.

Does the VA Directly Pay the Memory Care Bill?

No, the VA does not write a check directly to the memory care community. Instead, eligible veterans and surviving spouses can receive a benefit called Aid and Attendance. This is a tax-free monthly payment made directly to the recipient. You can use this money for any expense, making it a flexible way to help cover the monthly cost of memory care.

Are Memory Care Costs Tax Deductible in Ohio?

Yes, a significant portion of memory care costs can often be deducted as a medical expense on federal income taxes. The IRS allows for the deduction of costs for the diagnosis, treatment, and prevention of disease. Because a person is in memory care due to a medical diagnosis like Alzheimer's, much of the expense, including lodging and meals, often qualifies. A doctor must certify that your loved one is chronically ill and requires this level of care. Always work with a qualified tax professional to understand what you can deduct based on your specific financial situation.

Figuring this out alone is tough. The local advisors at Guide for Seniors help Cleveland-area families understand their options and find communities that fit their budget and care needs, all at no cost to the family. Get a personalized recommendation at https://www.guideforseniors.com.

Need Help Finding Senior Living in Greater Cleveland?

Our Greater Cleveland local advisors compare pricing, schedule tours, and answer your questions — completely free.