A Cleveland Family's Guide to Continuing Care Retirement Communities (CCRCs)

A Continuing Care Retirement Community (CCRC) is a unique type of senior living option that offers a full range of care—from independent living to skilled nursing—all on one campus. The main promise is that your loved one can age in place, moving seamlessly to a higher level of care if needed without the stress of finding a new facility.

-

TL;DR

-

All-in-One Campus: CCRCs combine independent living, assisted living, memory care, and skilled nursing in a single community. This prevents disruptive moves as health needs change.

-

Plan for the Future: Residents usually join while they are still healthy and active, securing guaranteed access to higher levels of care for the future.

-

Upfront Investment: These communities typically require a significant one-time entrance fee in addition to monthly service fees. Think of it as an investment in lifelong stability.

-

Contract is Key: The contract you sign determines your costs now and in the future. The three main types in Ohio are Type A (Life Care), Type B (Modified), and Type C (Fee-for-Service).

-

Peace of Mind: The goal is to eliminate the frantic, crisis-driven search for care that many families face when a loved one's health declines unexpectedly.

Disclaimer: This article is informational and not legal, financial, or medical advice. Please consult licensed professionals for case-specific guidance.

Understanding Your CCRC Options in Greater Cleveland

Alt text: Diagram showing four connected houses, illustrating the progression from independent living to assisted living, memory care, and skilled nursing within a CCRC.

Searching for the right senior living option in Greater Cleveland can feel overwhelming, especially when you’re stressed and short on time. This guide offers a clear, calm path to understanding CCRCs, one of the most comprehensive choices available.

Who this helps

This guide is for families in Cuyahoga, Lake, Lorain, Geauga, Medina, and Summit counties who are:

-

Planning for a parent or loved one's future care needs.

-

Stressed by the idea of moving them multiple times as their health changes.

-

Searching for a stable, long-term solution that provides peace of mind.

-

Comparing the costs and benefits of different senior living models.

Key takeaways

-

A CCRC, also known as a Life Plan Community, offers a full spectrum of care in one place, preventing future moves.

-

Residents typically enter while independent, with the assurance that higher levels of care are available if needed.

-

The financial structure includes a significant one-time entrance fee and ongoing monthly fees, which vary by contract type.

-

In Ohio, the contract you choose (Type A, B, or C) determines how you pay for future healthcare services.

How a CCRC Provides Lifelong Care on One Campus

The core promise of a CCRC is powerful: one move is the only move your loved one may ever have to make. These communities are designed to eliminate the stress of searching for a new facility when a health crisis happens.

Think of a CCRC like a neighborhood with different levels of support. A resident can start in an independent living apartment, enjoying social events and amenities. If they later need help with daily tasks, they can transition to an assisted living residence just a short walk away, staying within the same familiar community. This seamless structure provides stability for both residents and their families.

The Continuum of Care Explained

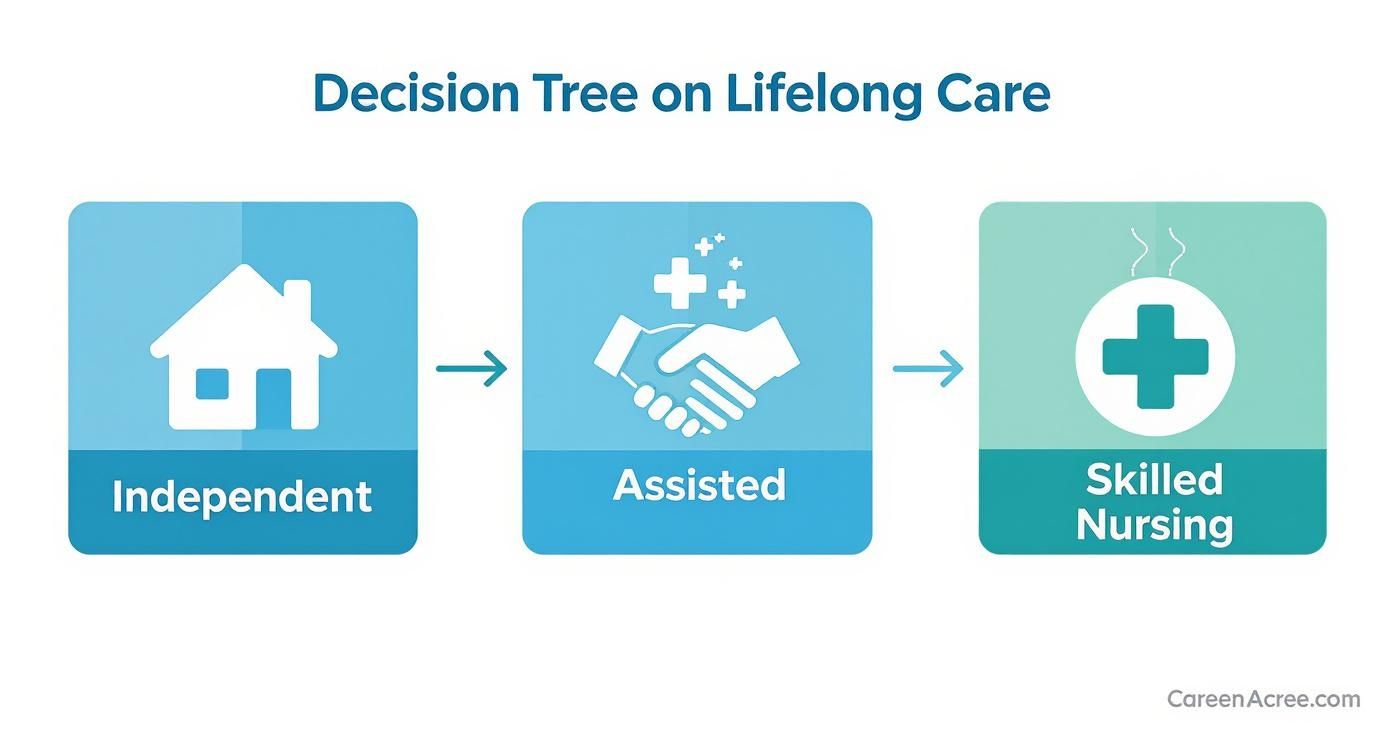

Here in Ohio, CCRCs offer a full spectrum of licensed care levels on one campus. This proactive approach to long-term planning ensures the right support is always available. Let's break down the typical levels of care you'll find.

-

Independent Living: The entry point for most residents. It offers an active, self-sufficient lifestyle in private apartments or cottages with amenities like dining, social events, and freedom from home maintenance.

-

Assisted Living (Residential Care Facility): When someone needs help with daily activities—like managing medications, bathing, or dressing—they can move to the assisted living part of the community. On first mention, it's important to know that in Ohio, these are licensed by the state as a Residential Care Facility. This means they meet specific care and staffing standards set by the Ohio Department of Health.

-

Memory Care: For residents with Alzheimer's or other forms of dementia, these specialized units provide a secure, supportive environment. Staff receive training in compassionate, person-centered care, often using practical tips for working with dementia patients. For more focused information, see our guide to memory care in Cleveland.

-

Skilled Nursing and Rehabilitation (Nursing Home): The highest level of medical care on campus. It's for residents who need 24/7 nursing supervision or short-term rehabilitation after a hospital stay. These facilities are regulated by both the state and the federal Centers for Medicare & Medicaid Services (CMS).

What This Means for Your Family in Cuyahoga County

Imagine your mother moves into a CCRC in Shaker Heights while she's healthy. A few years later, she falls and needs physical therapy. Instead of a disruptive move to an outside rehab center, she gets care right on campus in the skilled nursing wing. After recovering, she returns to her own apartment and friends. If her needs change again, assisted living services are ready. This stability is the true value of the CCRC model.

Choosing a CCRC means investing in this integrated system. You secure priority access to higher levels of care at a more predictable cost, all within a place your loved one calls home.

Navigating CCRC Contracts and Fee Structures

Understanding the finances of a CCRC comes down to two main parts: a one-time entrance fee and an ongoing monthly service fee.

The entrance fee secures a resident's spot and guarantees access to higher levels of care. The monthly fee covers daily services like meals, housekeeping, utilities, and activities. How these fees work together is defined by the contract you sign. This legal agreement outlines what you pay upfront, what monthly costs cover, and how costs might change as care needs evolve.

Alt text: Flowchart showing arrows connecting "Independent Living" to "Assisted Living" and "Skilled Nursing," representing the care continuum in a CCRC.

This planned path for future care is designed to prevent the stressful, last-minute scrambles so many families face.

The Three Main CCRC Contract Types in Ohio

In Ohio, CCRCs generally offer three contract types. Each balances what you pay now versus what you pay later for healthcare.

Type A: Life Care Contract

A Type A contract is the most comprehensive and predictable. It has the highest entrance fee and monthly fees, but it offers the greatest peace of mind.

-

How it Works: Residents pay an inclusive monthly fee that changes very little, even if they move to assisted living or skilled nursing.

-

Best For: Planners who want to lock in long-term care costs and protect themselves from rising healthcare prices. It acts like a private insurance policy for future care.

Type B: Modified Contract

A Type B contract is a middle-of-the-road choice. The entrance and monthly fees are usually more moderate than a Type A agreement.

-

How it Works: This contract typically includes a set amount of healthcare services, like a specific number of "free" days in the skilled nursing center per year or care at a discounted rate. After that, the resident pays the full market price.

-

Best For: Families comfortable with some calculated financial risk but who still want a safety net for future healthcare needs.

Type C: Fee-for-Service Contract

A Type C contract has the lowest upfront cost, with a smaller entrance fee and more affordable monthly payments for independent living. However, it carries the most financial uncertainty.

-

How it Works: You pay for healthcare services as you need them at the full daily market rate. The primary benefit is guaranteed access to that care without moving off-campus.

-

Best For: Families with a solid long-term care insurance policy or the financial assets to comfortably self-fund future care costs.

Comparing CCRC Contract Types in Ohio

This table breaks down how each contract type handles costs, helping you weigh what matters most for your family.

| Contract Type | Entrance Fee | Monthly Fees | Future Healthcare Costs | Best For |

| :--- | :--- | :--- | :--- | :--- |

| Type A (Life Care) | Highest | Highest | Largely prepaid; predictable | Families who want maximum cost stability and minimal risk. |

| Type B (Modified) | Moderate | Moderate | Partially covered (discounts or set days) | Families seeking a balance between upfront cost and future care coverage. |

| Type C (Fee-for-Service) | Lowest | Lowest | Paid at full market rates as needed | Families with LTC insurance or assets to self-insure future care costs. |

The right choice depends on your family's finances, risk tolerance, and goals. For typical pricing in our region, see our guide to senior living costs in Cleveland. Always have a financial advisor and an elder law attorney review any CCRC contract before signing.

Comparing CCRCs with Other Senior Living Options

When exploring senior living, you'll encounter independent living, standalone assisted living facilities, and dedicated memory care homes. So, where does a CCRC fit in?

A CCRC bundles all these options onto a single campus. Instead of choosing one level of care today, you invest in a community that guarantees access to every level of care your loved one might need later. This solves a common fear: having to move a parent again when their health suddenly changes.

Stability vs. Flexibility

The key difference between a CCRC and other options is long-term stability versus short-term flexibility. Standalone communities often have a lower initial cost but can't promise a resident can stay if their needs become too complex.

-

Standalone Assisted Living: In Ohio, these licensed Residential Care Facilities provide excellent support for daily activities. However, if a resident develops a condition requiring 24/7 skilled nursing care (which is CMS-regulated), they will have to move.

-

Standalone Memory Care: These communities offer incredible support for dementia but are not typically licensed for high-level medical care, which could force a move later on.

-

Continuing Care Retirement Community (CCRC): A CCRC is built for permanence. The on-site levels of care provide a stable home for life. This peace of mind comes with a higher initial cost (the entrance fee), but for many, that security is invaluable.

The global market for this growing market for senior care shows that more families are seeking this kind of long-term security.

A Head-to-Head Comparison

This table clarifies the key differences to help you compare your options in the Cleveland area.

| Feature | Continuing Care Retirement Community (CCRC) | Standalone Community (e.g., Assisted Living) |

| :--- | :--- | :--- |

| Care Progression | Seamless. Residents transition between care levels on the same campus. | Requires a move. If needs exceed the facility's license, the resident must find a new community. |

| Community Stability | High. Residents stay with their friends and familiar surroundings. | Variable. A move can be disruptive, leaving friends and routines behind. |

| Financial Model | Requires a large, one-time entrance fee plus monthly fees. | Usually a smaller community fee and monthly rent-style payments. |

| Cost Predictability | Higher. Type A contracts lock in future healthcare costs, protecting against market rate increases. | Lower. You pay for care as you go. A move to skilled nursing means paying the full market rate at that time. |

What This Means for You

Choosing a CCRC is like buying a comprehensive insurance policy for future care. A standalone community is more like a pay-as-you-go plan. The right path depends on your family's finances and how much you value lifetime stability.

Which Path Is Right for Your Family?

A CCRC is often ideal for planners—seniors who are still independent but want to make one decision to cover them for life. Standalone communities can be an excellent choice for immediate needs, especially when budget is a primary concern. To help weigh the factors, review our guide on choosing the right senior living option.

How to Finance a CCRC in Ohio

<iframe width="100%" style="aspect-ratio: 16 / 9;" src="https://www.youtube.com/embed/zZdybOdyCKU" frameborder="0" allow="autoplay; encrypted-media" allowfullscreen></iframe>Figuring out how to pay for a CCRC is a major question for families. It takes careful financial planning, but several routes can fund this investment in long-term peace of mind.

For many, the equity in their home is the key. Selling a long-time residence often covers most or all of the CCRC entrance fee. Personal assets like savings, investments, and retirement funds (401(k)s, IRAs) are also commonly used for both the entrance fee and monthly costs. A financial advisor can help create a strategy for drawing from these accounts tax-efficiently.

Using Long-Term Care Insurance

A long-term care (LTC) insurance policy can be a great help.

-

What it Covers: An LTC policy typically doesn't cover the entrance fee or independent living costs. It activates when a resident is certified as needing help with at least two "activities of daily living" (like bathing or dressing) and moves to assisted living or skilled nursing.

-

How it Works: The policy pays a set daily or monthly amount. Check the policy for the elimination period—a waiting period you pay for out-of-pocket before benefits begin.

-

First Step: Contact the insurance company to understand the exact coverage and claim process.

Veterans Benefits: VA Aid and Attendance

For wartime veterans and their surviving spouses, the VA Aid & Attendance pension can provide a valuable monthly payment to help with care costs.

-

Eligibility: This tax-free benefit is for veterans who require assistance with daily activities.

-

What it Covers: The funds can be applied to monthly fees for assisted living, memory care, or skilled nursing within the CCRC.

-

Example: A Veteran in Lorain County: A veteran living in an Elyria CCRC qualifies for Aid & Attendance. The monthly VA payment helps cover in-home care services in his independent living apartment, allowing him to stay independent longer before transitioning to the assisted living wing.

The Role of Medicare and Medicaid in a CCRC

Medicare and Medicaid have very specific and limited roles in paying for a CCRC.

-

Medicare: This federal health insurance does not pay for long-term assisted or independent living. Medicare Part A may cover a short-term rehab stay in the CCRC’s skilled nursing facility after a qualifying three-day hospital stay, but not long-term custodial care.

-

Ohio Medicaid: In Ohio, Medicaid generally does not cover independent or assisted living costs. If a resident spends down their assets, they may become eligible for Medicaid to pay for care in the CCRC’s skilled nursing facility, but only if that facility is Medicaid-certified. For the latest eligibility rules, check with the Ohio Department of Medicaid.

Your Essential CCRC Evaluation Checklist

Alt text: Two people reviewing a clipboard checklist titled "CCRC Evaluation," with items for financial health, contracts, and healthcare.

When touring a CCRC, it's easy to be impressed by the amenities. But it's crucial to look deeper. This checklist will help you gather the facts needed to make an informed decision.

Checklist for Your CCRC Tour

Use this list on every tour to compare communities fairly.

1. Financial Health & Stability

-

Occupancy Rate: Ask for current occupancy rates for all care levels. A rate of 90% or higher is a strong sign of a healthy, desirable community.

-

Financial Statements: Request their most recent audited financial statements to check for positive trends.

-

Fee Increase History: Ask for a 5-year history of monthly fee increases to help you budget for the future.

2. Contracts & Fees

-

Contract Type: Ask them to clearly explain if they offer Type A, B, or C contracts.

-

Refund Policy: Understand the entrance fee refund conditions. Is it prorated? What happens if your loved one moves out or passes away?

-

Level-of-Care Fees: Clarify how monthly fees change when a resident moves to a higher level of care. Level-of-care fees are additional charges for extra services in assisted living or memory care.

3. Healthcare & Care Transitions

-

Transition Process: Ask how a move between care levels is handled. Is there a dedicated care coordinator?

-

Staffing Ratios: Ask about staff-to-resident ratios in assisted living and memory care. For skilled nursing, cross-reference their answer with data on the CMS Care Compare website.

-

State Inspections: Request to see the most recent state inspection report from the Ohio Department of Health. They are required to make this available to you.

Example Scenario: Cuyahoga County family using the AL Waiver

A family in Parma is considering a CCRC for their father, who may soon need assisted living. They learn he might qualify for the Medicaid Assisted Living Waiver (AL Waiver), which helps cover care costs in an assisted living facility. They ask a CCRC if its assisted living wing accepts the AL Waiver. The community confirms they do, which significantly impacts the family's financial planning. Always ask if the community accepts the specific benefits you plan to use.

What to Do Next

-

Discuss as a Family: Have an open conversation about long-term wishes and what is financially realistic.

-

Gather Financial Documents: Collect documents on assets, income, and any long-term care insurance policies to understand your budget.

-

Schedule Tours: Use the checklist above to tour at least two different CCRCs to compare them effectively.

-

Consult Professionals: Before signing any contract, have it reviewed by an elder law attorney and a financial advisor.

FAQ: Common Questions Cleveland Families Ask

What if spouses need different levels of care?

This is a key strength of the CCRC model. One spouse can live independently while the other receives care in assisted living or memory care, all on the same campus. This keeps them close and simplifies visits.

Can we use Medicare to pay for the CCRC?

Mostly no. Medicare does not pay for room and board in independent or assisted living. It may cover a short-term, rehabilitative stay in the skilled nursing facility after a qualifying hospital stay, but it is not a long-term payment solution.

Is the entrance fee tax-deductible?

A portion of the entrance fee and monthly fees may be considered a prepaid medical expense and therefore tax-deductible. This depends on your contract and financial situation. Consult a tax advisor for guidance.

What if we run out of money?

Many reputable non-profit CCRCs have a resident assistance or benevolent care fund. These funds are designed to help residents who have outlived their assets through no fault of their own. Be sure to ask about this during your tour.

For CCRCs looking to connect with families, mastering local SEO strategies is crucial for appearing in local search results.

Need Help Finding Senior Living in Greater Cleveland?

Our Greater Cleveland local advisors compare pricing, schedule tours, and answer your questions — completely free.